This is part of a series of posts on 10 Important Financial Lessons To Learn While You’re Young. A new lesson will go up every Friday. And if finances bore you, don’t worry…I’ll keep posting non-finance things on Mondays!

Ok, I changed my mind. You still get bonus points if you decided to make a budget after reading last week’s lesson, but now I’m going to say you really should do it anyway. :-p

Budgeting is not hard, but it is something that takes some effort to learn and maintain. The basic principle is simple: to create a budget you should track your income, track your expenses, and don’t spend more than you make. But we’ve been trying to stick to a budget for a little over a year (about as long as we’ve been tracking our spending) and I’m only just now feeling fairly confident about my budgeting plan. The problem was I jumped right in and tried to “stick to” my budget without even being sure that I had a workable/reasonable budget.

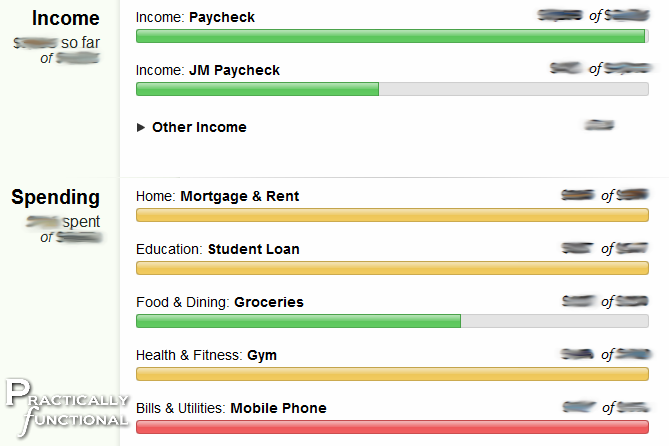

We use Mint (which is free!) to create our budget. I love it because it automatically connects to our bank accounts and credit cards, pulls in all of our transactions, and even attempts to categorize them for us (though sometimes it makes some fairly hilarious mistakes! It always wants to categorize Bar Method, my exercise class, as “Alcohol & Bars”). Then it keeps track of each category, how much we’ve spent, how much is left, etc.

|

| We went $1 over in “Mobile Phone” so it gave us this big red angry bar! |

But if you’re just starting out my suggestion is to start with baby steps. For your first budget use only four categories:

- Income: This is your income, duh. But make sure this category includes all your income, not just your regular paycheck. You should count tax refunds, gifts, side job income, etc. The only income we purposely leave out is interest income from our banks because it’s such a small and varying amount.

- Needs: You can be fairly flexible on what is included in this category (and in the Wants category) but try to be reasonable. Obviously you should include money spent on rent or mortgage and groceries. Utilities. Insurance. What counts as a need varies from household to household, but these should be the most important things, the things you really couldn’t do without (without a major lifestyle change). For us, our cell phones count here, but our gym membership doesn’t. :-p

- Wants: This should be pretty much everything else you want to spend money on that didn’t fit into the needs category. And this is where you should cut expenses if you need to cut them down one month.

- “Allowance”: This is actually a fairly important category for us. The idea is that sticking to a budget can be super hard, and you’re not going to be successful if you don’t give yourself a bit of leeway. So we make sure to set aside a little bit of money for each of us each month that we can spend on whatever we want. It doesn’t have to fit into any category and we don’t have to be accountable for it. If I wanna spend my allowance on Starbucks and shoes I can, dammit!

By the way, Lesson 5 is going to touch on savings, which will be it’s own category somewhere between Needs and Wants. More on that later!

One very important thing to remember about your budget is that it will change month to month. I didn’t realize this at first and spent many months beating myself up for it. Our spending was never the same month to month and it freaked me out because I had to keep changing the budget when we went out to eat an extra time or spent more at Michael’s than the previous month (damn craft habit!)

What I finally realized is that if I took our twenty or thirty specific spending categories and grouped them into the larger categories of Wants versus Needs, our spending on Needs was mostly the same each month. It was the spending on Wants that varied so much. It was a nice realization because, besides eliminating some of the stress I felt about the budget changing so often, it also eliminated some of my worries about what we were going to do if we ever needed to cut back on the budget. There’s a big ol’ chunk of Wants that can be reduced before we even have to worry about starving!

So that’s it, just split everything you earn or spend into one of those four categories. If you want to get more detailed later, you can divide those four categories further like we did. (Maybe I’ll write a more detailed post later about how we use Mint for budgeting.) But always make sure you still know the difference between your needs and your wants. At some point you will probably need to cut your budget back for some reason or another, and you need to make sure to do it from the right places.

Do you already have a budget? How’s that going? Have you tried to make one before, but had a hard time like we did? Do you use a different budgeting strategy? (I keep hearing about the envelope method.)

Katie says

Yes, it was miserable trying to estimate things when we were being paid hourly! Definitely easier when you know exactly how much you'll be getting and when.

That's a good idea, to split up the annual costs of things. We pay our car insurance monthly for that reason, but I hadn't thought about things like the car tag…now that mine's due in two months. ^_~ Theoretically I'd like to do that for things like Christmas presents, too, but it seems like right now we're just shoving everything we have at the debt and the random expenses just surprise us. Oh well.

Jessi W says

So, to tell the truth I definitely simplified our budgeting process in this post. I wanted to just get it out there that you should have a budget, an easy way to start is Mint, etc. But like you I have about ten different spreadsheets (Excel for the win!) for tracking stuff.

The biggest difficult, at least for me, is that JM's pay is variable, he's paid hourly. So our income differs every month depending on how much he works, so I have a spreadsheet out there to calculate his pay based on expected hours, taxes withheld from paychecks etc. (plus about 9 others for other various pieces).

One other thing we do that I have found super helpful is we try to estimate yearly costs for things, then split them down into portions for each month. For example, we know how much renewing the registration will cost each year for the car, so we split that total by 12 and set aside $X each month into a savings account so that we aren't blindsided by an "extra" expense in January. It's sort of like the envelope method of budgeting, but you could do that for groceries too maybe.

And I agree, seeing how other people do budgets is fascinating, so thanks for sharing!

Katie says

One of my biggest problems with sticking to our budget is the mindset that, well, I've gone over the budget with this one purchase so I guess the whole thing's shot and I'll just keep spending money.

I used to use Mint, but the problem is that using cards really encourages me to overspend. I just can't seem to stick to a budget with them. So I withdraw the amount of cash my budget tells me I can spend and leave my debit and credit cards at home (except when I need to buy gas, because Sam's only takes plastic at the pump).

So instead of Mint, we have a few spreadsheets worked out. The first is a straight income vs. expenses one covering an entire month: here is how much Hyphen makes, here's how much I make, here are all our bills and the amounts we need to pay on his student loans and the debt from when he was unemployed, etc.

Then on a separate spreadsheet I broke that down into a "Monthly Spending Plan" based on when we actually get our paychecks. Hyphen gets paid at the end of each month and his check covers the mortgage, the utility bills, the cell phone, the student loans, and the cc debt. I get paid bi-weekly and I have it broken down into: I need to pay the car payment out of this check because it's due in the first half of the month; the car insurance out of the second one because it's due at the end of the month; etc. The grocery/allowance/savings money (these are my flexible categories that change each time because they're essentially a division of what's leftover after everything else is paid) all comes out of my checks, and I also have a set amount that I transfer into Hyphen's account to help pay off the debt.

Then I copy that spreadsheet for each month and I can rework it for each paycheck. So this month we had an extra expense here so I'll trim from the grocery/savings budget or we had some bonus income there and it can go toward the loans, etc.

Finally, and this is the one I'm worst about, I have a spreadsheet for each paycheck with my grocery budget and how much I plan to spend on essentials, so I have an idea on how much there might be leftover to use for eating out or whatever. I can put in the amount of my co-op food order ahead of time, and I use an app on my phone for a shopping list and track how much things like dog food cost–so I know that if we'll need to buy it in the next two weeks, I need to reserve $41.26 out of that grocery budget for dog food. The problem is I'm less good about entering in the amounts of money I actually spend to track the difference between the budget and reality…I'm working on it, though.

And since it's all Google spreadsheets, I can hop on them at work or home and we can share them to see what we're doing. ^_^

You are so right about needing to grant yourself an allowance! I just have the "grocery" budget that needs to buy food, household goods, pet supplies, and then extra can be spent on eating out or stuff for me. I also had to start giving Hyphen an allowance just for his spending because he kept putting things on his credit cards–little things like QT coffee or donuts or picking up butter on the way home, but they would all add up and he was always surprised by how much he had spent by the end of the month.

Anyway, sorry for replying to your blog post with a blog post of my own! It's interesting to see how other people do budgets. They're so fascinating and awful at the same time!